Volatility sets in as growth momentum rolls over

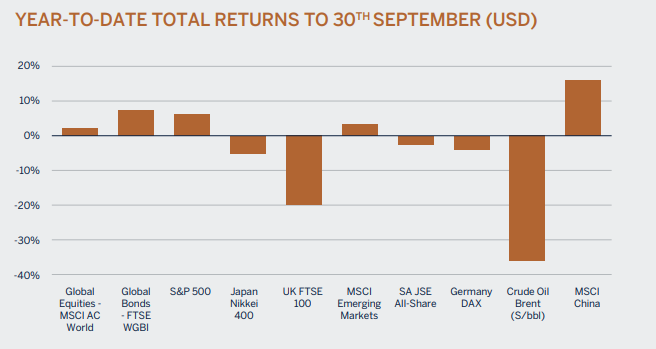

2020 has truly been a roller coaster ride and has tested the nerves of even the most experienced and sanguine of investors. After one of the sharpest and swiftest market sell-offs and severest and deepest recessions in history, global equity markets, as defined by the FTSE All World TR Index, have rebounded by more than 50% from their lows seen in March leading the index to be in positive territory on a year to date basis. Indeed, very unusual, but a function of the sheer magnitude of fiscal and monetary policy stimulus measures implemented to stave off what could have been a much more prolonged and painful recession. However, not all markets have recovered with the UK FTSE All Share TR disappointingly still nearly -20% year to date whilst investment markets also lost some steam towards the end of the third quarter as certain forward[1]looking growth indicators in the services sectors (predominantly hospitality and tourism) trended lower in regions that experienced an increase in coronavirus infections.

A resurgence of infection rates led to economic headwinds as the re-introduction of social distancing measures were implemented in these regions. Furthermore, risks to additional fiscal policy support have increased in the US as the House Democrats and White House couldn’t agree on the terms of additional income support for individuals and small businesses that were negatively affected by the lockdown measures. This has raised concerns about an abrupt slowdown in consumer spending which will make the prospects of a full recovery even more distant.

Source: FactSet

Will COVID-19 derail the global economic recovery?

In short, we don’t think so, at least not permanently. We do however concede that the world will most likely have to adjust and learn to live with COVID-19 and its lasting effects in one way or another.

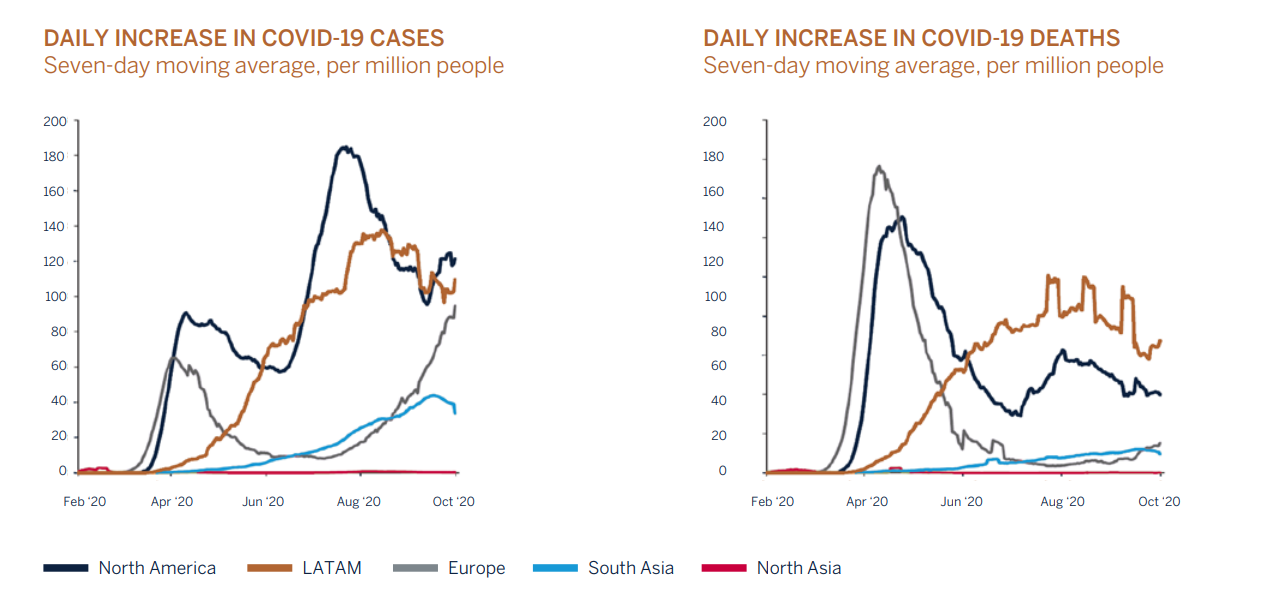

COVID-19 cases are on the rise again and expected to spread faster with the arrival of cold weather in the northern hemisphere. This is not a surprise given that a working vaccine is not yet available and lockdown measures were relaxed during the summer months which resulted in an enthusiastic response by many younger individuals. Certain countries and sectors will unfortunately be more negatively affected than others. Southern Europe as an example is very sensitive to the tourism and hospitality industries, and the re-introduction of restricted measures to curb the spread of the virus will inflect serious pain on companies and sectors that were already experiencing financial difficulty during the first wave of the virus. Government will have to step in again to ensure that many of these companies remain solvent and in operation. In the near term these events are expected to slow down the pace of recovery as is already evident from high frequency mobility data in countries most affected. Investors should however not lose sight of the fact that the above-mentioned measures should be viewed as necessary, but importantly also transitory in nature and are therefore not expected to derail the global economic recovery which is currently fuelled by unprecedented monetary and fiscal policy interventions.

Source: JPMorgan Asset Management

The good news is that although cases have been increasing at a brisk pace a significant component of the increase can be explained by an acceleration in testing. In addition, the fatality and hospitalisation rates are currently a fraction of what they were earlier this year because new infections are skewing towards younger and less vulnerable populations, with the result of much less pressure on healthcare systems. At the same time, older (and less economically active) individuals appear to have been self-shielding, as they recognised the increased risk they face. Medical treatments for COVID-19 have also advanced rapidly and played an important role in reducing the severity of illness and mortality rates. Collectively these are important developments which will reduce the pressure on politicians to enforce the same draconian measures that were implemented during the onset of the pandemic when the motivation at the time was to limit pressure on healthcare systems and prevent increases in mortality.

It is therefore highly likely that governments will accept modest levels of infection cases as a necessary cost for maintaining a certain level of economic activity. This is especially the case now given that the current wave of infections looks very different given that the majority of cases are either mild or asymptomatic, which allows governments to be more specific in their approach towards containing the spread of the virus, instead of implementing broad based shutdowns of economic and social activity.

The discovery and approval of a successful vaccine/s as a means to strengthen herd immunity levels will be a game changer and assist in speeding up mobility rates and in turn the economic recovery and news on this front has been rather encouraging. Vaccines normally require around a decade to become operational but given the pressured timeline it is now expected that a vaccine could be approved as early as next year. Even though there is sure to be manufacturing and distribution challenges that will need to be overcome, the approval of a vaccine bodes well for a sustained improvement in economic activity and there is increased confidence that this will materialise sometime in 2021. In the interim with real growth expected to be lower equity investors must expect increased levels of volatility and lower returns going forward whilst they will have to be increasingly selective in their investment making decisions.

The abrupt change in direction in investment markets is a reminder of just how fragile and dependant financial markets have become on stimulus measures as well as the outlook for COVID-19 infections, but it also highlights the importance of being patient and selective when making investment decisions as growth in the future will likely be more constrained in a world with bloated balance sheets and a change in consumer behaviour given COVID-19.

The combination of elevated valuations across all asset classes (a function of low interest rates), uncertainty surrounding the up-coming US presidential elections, prospects of a hard BREXIT, and a slowdown in growth momentum due to a pick-up in infections and the removal of fiscal support are sure to provide a fair dose of volatility in the near term. Volatility does however provide investment opportunities, and investors will do well to stay the course and focus on the fundamentals which have been improving as the global economic recovery takes hold (even though it may be bumpy at times) and not be swayed by the short term noise which at times can be overwhelming.

Our investment approach, irrespective of the environment, is to focus on fundamentals while assessing the risks that we are being presented with, and to not be influenced by daily market movements or momentum. We will continue to ensure that portfolios are adequately diversified to navigate through what could be a more volatile period lying ahead of us as the year draws to a close.

Investment Performance

Despite a weaker end to the quarter and being marginally underweight equites client’s global USD and GBP multi-asset portfolios enjoyed another strong period aided by gains in global equity markets. However, again the UK FTSE All-share TR index lagged falling by -2.92% for the summer period leading to a decline of just under -20% year to leading domestic GBP portfolios to once more struggle on both a relative and absolute basis for the quarter and year to date. We continue to actively adapt underlying investments towards companies that remain well positioned to both survive and prosper despite COVID-19. Fixed income mandates were flat to slightly positive during the period and were broadly in-line with benchmark. On a year to date basis positive returns have been delivered although some underperformance has been seen due to our ongoing cautious short duration strategy as risk/return metrics appear unfavourable.

Asset Classes

| Equities | Neutral |

| Fixed Income | Underweight |

| Cash Plus | Overweight |

Asset Allocation

We have recently made use of volatility in investment markets to tactically increase the equity exposure to Neutral from a one notch underweight position previously. The change in allocation was primarily driven by our belief that following recent central bank comments interest rates will be held low for a prolonged period and continue to provide an underpin to valuations while the economic recovery takes hold. Following its latest meeting the US Fed has indicated that they expect interest rates to remain unchanged until 2023 and signalled that the tolerance to inflation has become more balanced, given their “new” 2% average inflation targeting objective accompanied by maximum employment. This view is very much supported by central banks globally. The outlook for earnings growth has also improved in line with economic fundamentals, with an expectation of a strong rebound over the next year. Although we don’t expect future returns to be in line with the expected recovery in earnings given the already strong recovery in share prices, we would expect the asset class to outperform both cash and fixed income securities over the next year.

Government and corporate bonds have been, and still are, very much supported by the aggressive buying from developed market central banks, which has in turn resulted Asset Classes Equities Neutral Fixed Income Underweight Cash Plus Overweight Bernard Drotschie / Chief Investment Officer in much lower market interest rates and strong growth in liquidity as measured by money supply. These measures will probably continue for a while longer and have served their purpose in providing companies access to liquidity as well as lowering the cost of funding to record low levels. Although these events bode well for borrowers, that is not necessarily the case for bond investors who will be receiving unusually low to negative absolute and real yields on their capital. We are comfortable to maintain a maximum underweight position to developed markets bonds. In addition, volatility this year has afforded us an opportunity to cautiously accumulate Credit and High Yield in the fixed income strategies to enhance returns.

The neutral position in global equities and maximum underweight in fixed income have left portfolios with an overweight position in cash, which serves as a risk mitigator in portfolios. In addition, the overweight cash position will provide us with ample capital to deploy when more favourable conditions or valuations present themselves.

Equities

|

Consumer Discretionary |

Overweight |

|

Consumer Staples |

Neutral |

|

Energy |

Underweight |

|

Financials |

Underweight |

|

Healthcare |

Overweight |

|

Industrials |

Neutral |

|

Information Technology |

Overweight |

|

Materials |

Neutral |

|

Consumer services |

Neutral |

|

Utilities |

Neutral |

|

Real Estate |

Underweight |

With the global economy unlikely to be firing on all cylinders for quite some time, a valuation premium will continue to be assigned to those companies that can sustainably grow their earnings. This is particularly the case in a world where almost every industry is being disrupted by a reshaped competitive landscape. Our investment philosophy focuses on identifying the winners.

We are mindful about the high valuations attached to quality growth stocks. Trees don’t grow to the sky, and neither do share prices. The risk of overpaying or being blindsided by the unexpected is mitigated in client portfolios through:

/ A conservative bias when making long-term earnings projections.

/ Healthy scepticism about assigning higher “it’s different this time” valuations relative to history.

/ Purposeful diversification by sector, theme and geography.

In other words, we guard against falling in love with a successful investment by constantly challenging its place in the portfolio and by incorporating a margin of safety in our analysis.

Amphenol is a recent purchase. The company manufactures connectors that are critical for ensuring power is transmitted in an electronic circuit. It is easy to see the secular growth in “connectedness” continuing for many years and decades to come as a result of the proliferation of electronics in more and more products. Crucially, it is nigh impossible to displace Amphenol’s mission-critical components once they have been designed into a product. In addition, the company is highly diversified by end markets, making it less obviously prone to rapid technological disruption. All these strengths are evidenced by a consistent and long track record of strong cash flow growth.

Fixed Income

|

G7 Government |

Underweight |

|

Index-Linked (US Government) |

Overweight |

|

Investment Grade - Supranational |

Overweight |

|

Investment Grade - Corporate |

Overweight |

|

High Yield |

Overweight |

Economic data releases have been upbeat but past activity does not guarantee a lasting theme – at least at the current pace, which remains flattered by recoveries from depressed down levels. The Federal Reserve recently tweaked their mandate with regards to inflation and now seek that it ‘averages 2% over time’. This has implications for the interest rate outlook, signalling that rates will remain unchanged even if faced with inflation rising above target. Near-zero interest rates and the ongoing pandemic should, in theory, add to the attractiveness of the government bond market but yields at current levels have factored much in and allow little in the way of a safety net in the event of higher inflation and an ongoing economic recovery. Vast money supply creation may contribute to higher inflation in 2021 and if vaccine hopes becomes reality, a ‘risk on’ mood should pervade. If this unfolds and the economy successfully navigates this terrible episode, then attention will quickly turn to an eventual dialling down in stimulus measures. This could be particularly damaging to government bond yields which at current levels are not priced for this scenario. As such, we remain defensively positioned with respect to duration as only marginally higher yields on longer-dated debt are not nearly enough compensation for the added risk.

In the UK, the sugar-rush from stimulus measures and easing of lockdown restrictions seems to be running out of steam. Whilst key economic data releases point to a healthy expansion, albeit from a very low base, more recent indicators for both the manufacturing and the service sectors are off the highs experienced in July. There is no doubt that the potential for the recovery to slow, or even stall, has risen following the Government’s new restrictions as Covid-19 cases again climb. The Monetary Policy Committee (MPC), continue to hold interest rates near zero, however there is increased speculation that the MPC may, at some stage, implement negative rates. We are not yet convinced, the lesson from Germany is that this highly unconventional policy can be very difficult to reverse and can quickly have diminishing positive effects. However, it appears the bond market has already made up its mind on this matter with UK Gilt yields already trading in negative territory out to seven years in maturity. Negative or not, we do know that an almost zero interest rate policy will be with us for quite some time.

The recovery in Investment Grade (IG) and High Yield (HY) corporate bond markets has been dramatic following severe capital declines in March and spreads are edging closer to pre-COVID levels which certainly doesn’t appear to make them look cheap. However, the environment for both taking risk and yield hunting remains supportive. Central bank initiatives have increased the allure of riskier fixed income assets and those that can pay an income stream above government debt are greatly benefitting as the world remains starved of yield. One could argue that the global marketplace’s reliance and in many respects complacency towards central bank support is possibly creating a bigger issue down the road, and this is entirely plausible. However, the past six months has clearly demonstrated the pitfalls of being too risk averse in an environment where the central bank ‘has your back’. We continue to hold IG debt with a smaller allocation to HY in our fixed income strategies and any upcoming weakness may persuade us to increase weightings to both.

Currencies / Interest Rates

RECOMMENDATION - INTEREST RATES

|

Current |

Direction |

||

|

US Dollar |

Overweight |

0.25% |

→ |

|

Sterling |

Neutral |

0.10% |

→ |

|

Euro |

Underweight |

0.00% |

→ |

The US dollar has posted a negative quarter with virtually all of the downside attributed to the month of July. Ultimately, the currency was due a period of consolidation but where do we see direction from here? Firstly, it is important to appreciate that the currency, in general terms, is only down approximately 2.5% year-to-date and in fact, the relative outperformance of the US bond market versus the German bond market (as an example) has more than compensated for the currency’s depreciation against the Euro. Without doubt, the outlook for the US dollar is negative if other developed economies (Eurozone, UK etc.) enjoy periods of economic ‘catch-up’ but we are not currently seeing enough evidence of this. The US still enjoys a solid advantage in this arena and is backed up by a central bank that seems willing to pull out all the stops to stimulate growth. The US dollar has defied the ‘demise of the dollar’ story time and again, and whilst it may well be different this time, it will not be a one-way street. It is crucial to remember both the performance and yield (often negative) of the asset class underlying each respective alternative currency – we remain overweight for now.

Sterling has been somewhat resilient over the quarter gaining approximately 4% against the US dollar, although more recently has given up some ground from the September high of $1.34. Sterling strength has been more attributed to US dollar weakness rather than broader support for the currency as it struggled to rise against other currencies, especially the Euro. We have commented for some time that Sterling is undervalued on a purchasing parity basis and over the long-haul, should regain some footing. However, current headwinds from the resurgence of BREXIT uncertainties, particularly with year-end deadline fast approaching and still no deal in sight, combined with heightened restrictions to control the increasing spread of COVID -19 is likely to keep volatility elevated. Our Sterling International fixed income strategies remain moderately overweight base currency, but it is still too soon to exit the foreign currency exposure which sits as a hedge against potential shorter-term weakness.

Market Performance % / as at September 2020

|

EQUITIES |

Q3 |

YTD |

12 MONTHS |

|

Global |

|||

|

FTSE All World TR Net (Sterling) |

3.30% |

3.68% |

-5.15% |

|

FTSE All World TR Net (US Dollar) |

8.08% |

1.18% |

-10.31% |

|

UK |

|||

|

FTSE All-Share TR |

-2.92% |

-19.92% |

-16.59% |

|

US |

|||

|

S&P 500 TR |

8.93% |

5.57% |

15.15% |

|

Europe |

|||

|

Dow Jones Euro STOXX TR |

0.67% |

-10.95% |

-6.19% |

|

FIXED INCOME |

Q3 |

YTD |

12 MONTHS |

|

Bloomberg Barclays Series - E UK Govt 1-10 Yr Bond Index |

-0.08% |

3.01% |

1.69% |

|

Bloomberg Barclays Series - E US Govt 1-10 Yr Bond Index |

0.19% |

6.02% |

6.03% |

|

JP Morgan Global Government Bond (Sterling) |

-2.00% |

9.91% |

1.70% |

|

JP Morgan Global Government Bond (US Dollar) |

2.54% |

7.25% |

6.69% |

|

Iboxx Sterling Corporates Total Return Index |

1.55% |

4.49% |

4.29% |

|

Iboxx US Dollar Corporates Total Return Index |

1.57% |

6.53% |

7.73% |

|

CURRENCY vs. STERLING |

Q3 |

YTD |

12 MONTHS |

|

US Dollar |

-4.12% |

2.68% |

-4.81% |

|

Euro |

-0.04% |

7.32% |

2.34% |

|

Yen |

-2.03% |

5.72% |

-2.43% |

|

CURRENCY vs. US DOLLAR |

Q3 |

YTD |

12 MONTHS |

|

Rand |

4.26% |

4.54% |

7.51% |

|

Euro |

2.19% |

2.95% |

2.49% |