Changing landscape under Trumponomics 2.0.

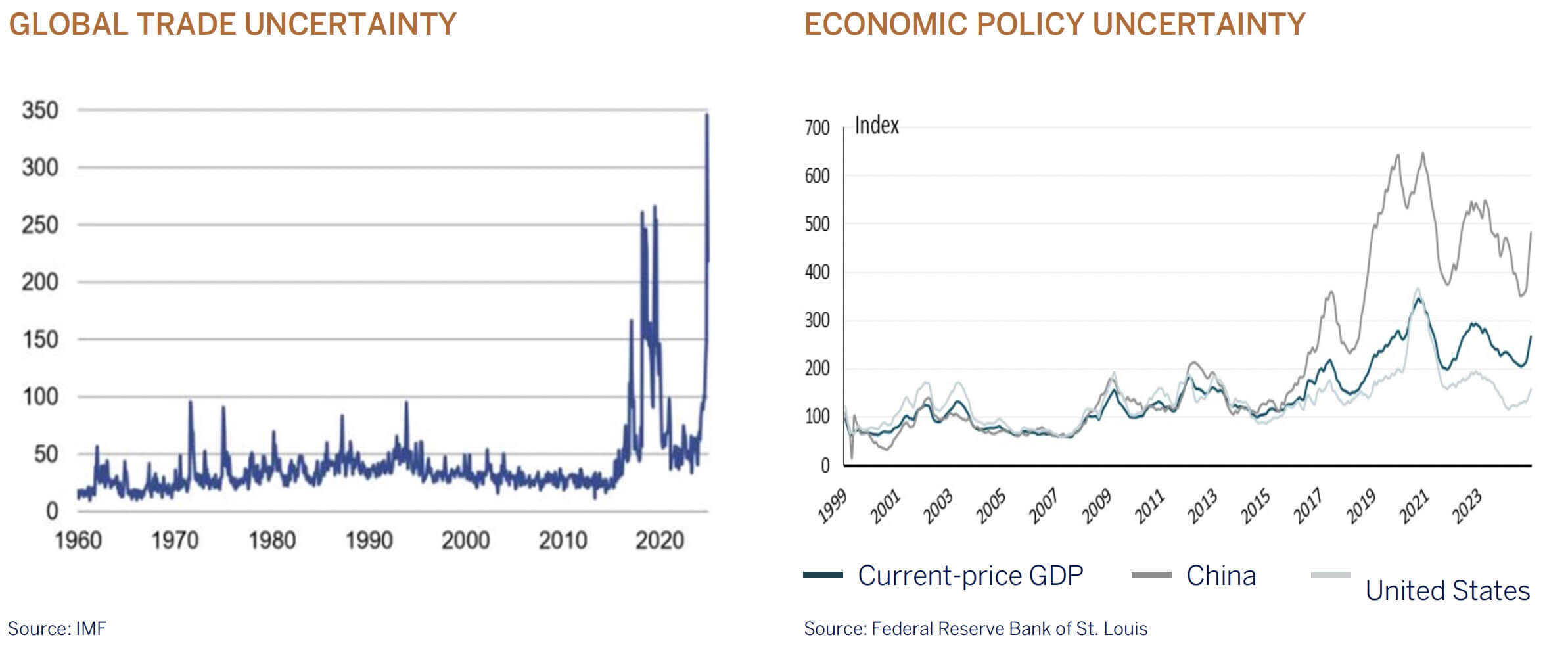

The first quarter of 2025 was marked by significant volatility across global financial markets, driven largely by the US President Trump’s administration’s proposed policies aimed at “making America great again.” In particular the erratic deployment of trade tariffs and the US Administration’s more onerous than expected import tariff announcements on “Liberation day” with threats of retaliation, have created elevated levels of policy uncertainty and deep rooted concerns over their effects on the global economic outlook for the rest of the year.

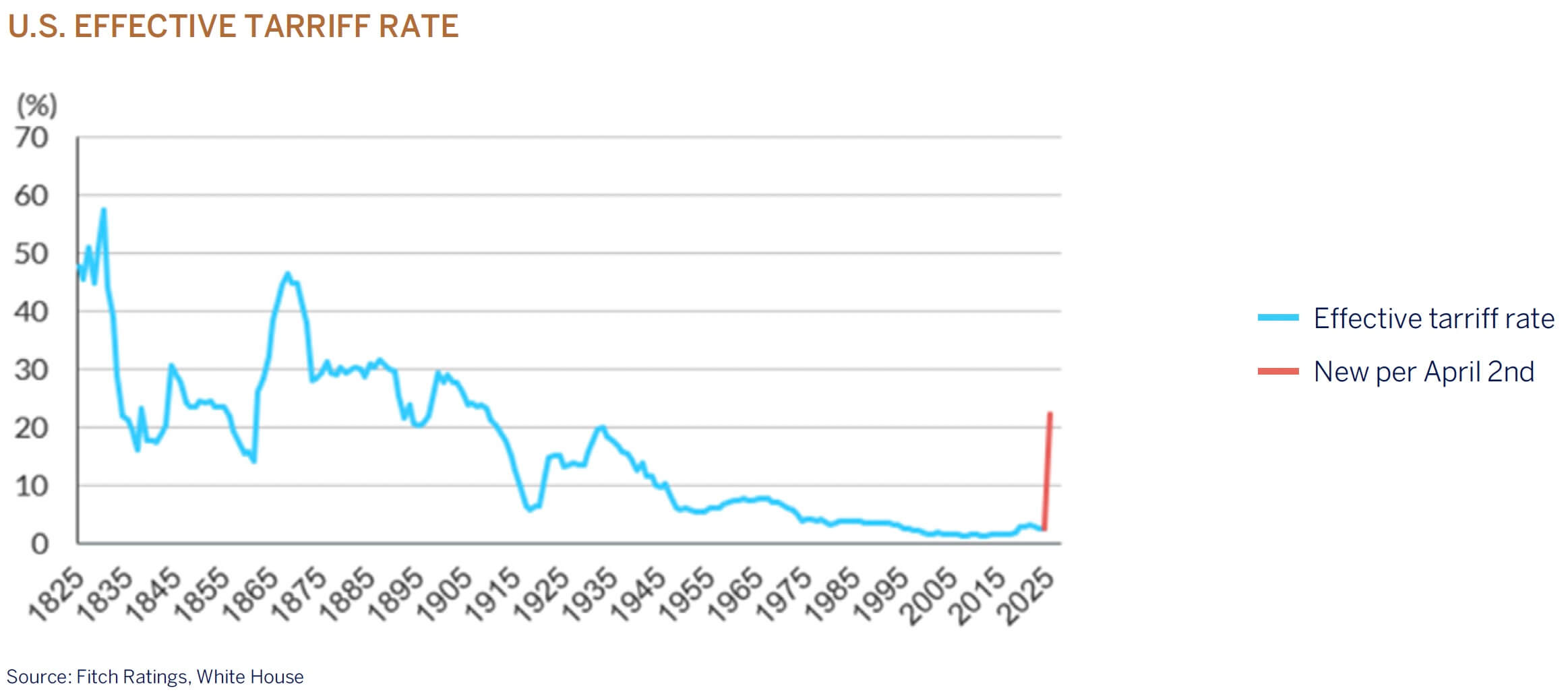

President Trump announced a significant shift in US trade policy, introducing a minimum baseline tariff of 10% on goods imported from all foreign countries. Additionally, higher “reciprocal tariffs” will be imposed on nations that levy tariffs on US exports. These measures are set to take effect on April 5 and April 9, respectively. If implemented, the effective US tariff rate is expected to approach 25%.

"extreme levels of policy uncertainty and heavy tariffs are meaningful economic headwinds that will likely cause ongoing volatility in asset prices."

Applied to a base of $3.3 trillion in US goods imports, this year’s cumulative tariff hike should be viewed as a substantial tax increase of approximately $660 billion, or 2.2% of GDP. While these changes aim to bolster American industry and reduce the national debt, they also raise concerns about potential price increases for consumers and disruptions in global trade. The impact on inflation could be significant, potentially adding nearly 2% to headline inflation.

The US seems to be hoping that by implementing tariffs it will be able to force concessions from other countries in return for lowering them. Time will tell, but in the short term, extreme levels of policy uncertainty and heavy tariffs represent meaningful economic headwinds that will likely cause ongoing volatility in asset prices.

"Trump has indicated that 'short-term pain' may be necessary for long-term gains."

Whilst the US economy looks set to benefit from lower taxes and deregulation in the medium term, the uncertainty over tariffs and the accompanying risk of higher inflation have significantly impacted both consumer and business confidence so far this year, raising concerns about potential stagflation. Indeed, the US Federal Reserve (Fed) now expects a combination of moderately lower economic growth and higher inflation in the near term, likely resulting in the Fed being forced to hold interest rates higher for longer as it attempts the difficult balancing act of containing renewed inflation risks without tipping the economy into recession. Investors will need patience as the world adapts to the changing landscape under Trumponomics 2.0.

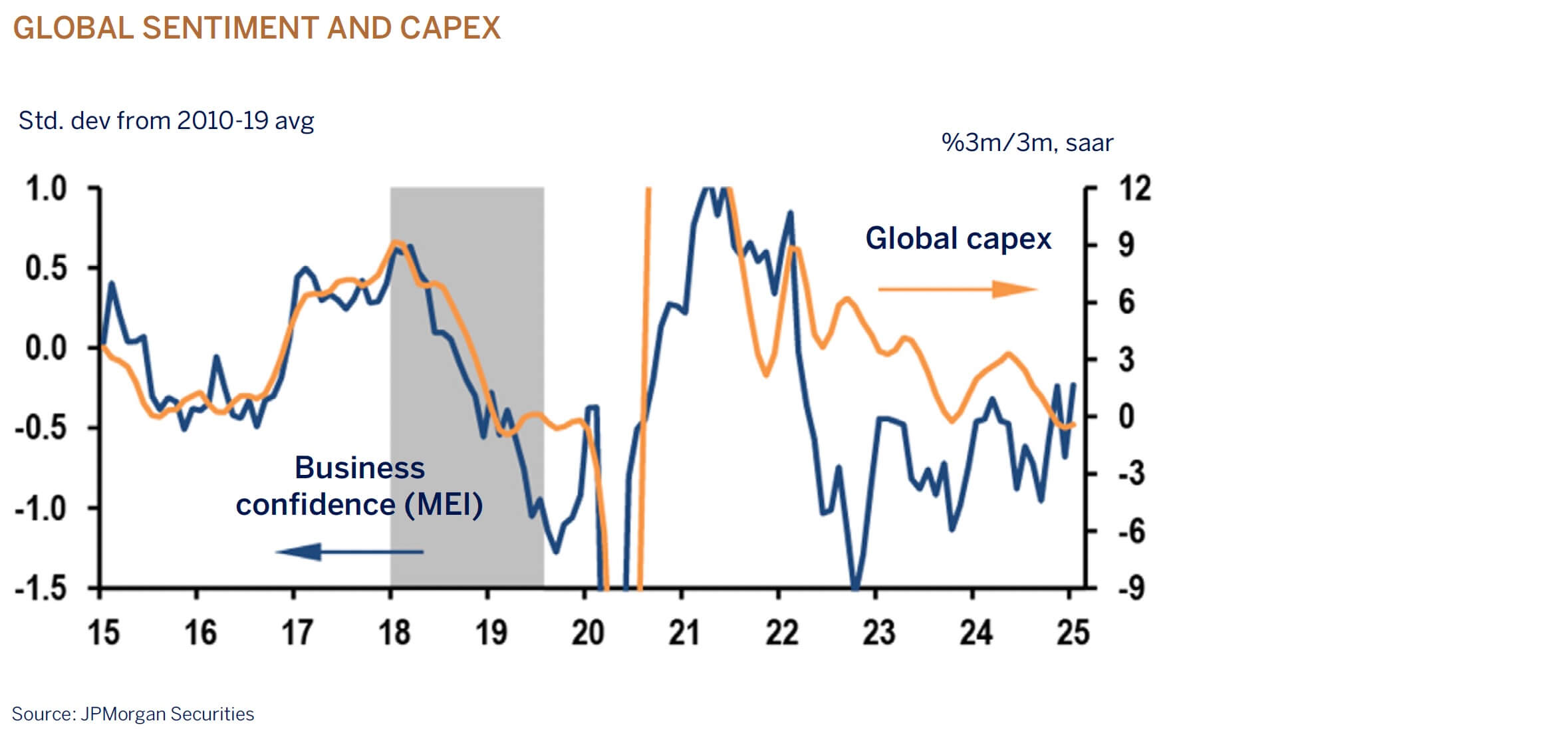

Despite generally resilient economic data year-to-date, markets have been pricing in the prospect of companies delaying investment and hiring until the new administration’s policies are clear. While Trump has called tariffs “the most beautiful word in the dictionary” and views them as a useful tool to negotiate favourable terms for the US, the risk is that retaliatory actions by its largest trading partners could escalate into a more economically damaging global trade war. This would have far-reaching implications as companies adjust their supply chains or relocate their manufacturing facilities. Recent IMF research suggests that a 10% increase in tariffs on all US imports, followed by 10% retaliatory tariffs on US exports, could reduce global growth (gross domestic product – GDP) by 0.5%, with the US bearing the brunt. The impact on GDP from supply chain adjustments is harder to quantify, but President Trump has indicated that “short-term pain” may be necessary for long-term gains—a factor perhaps not yet fully priced into financial markets.

While disruption in global trade is expected, it should be noted that businesses have strengthened their resilience since the Global Financial Crisis, Trump’s first term, and COVID-19, enabling them to navigate uncertainties more effectively. Many companies anticipate minimal impact due to diversified supply chains, a “local-for-local” manufacturing model, and proven disruption management. Currency movements will offset some effects, and tariffs will be managed through pricing strategies. Growth plans will focus more on increasing volumes rather than raising prices. Outside of the technology sector, companies remain cautious on capital expenditures, prioritizing debt reduction and returning surplus capital to shareholders.

In conclusion, while the proposed policies are introducing short-term challenges, businesses are better equipped to manage uncertainties. We will continue to monitor developments closely and focus on investing in well-managed global companies that are best positioned to adapt to the evolving environment, while keeping a close eye on broader economic trends.